Understanding the New GST/HST Rebates for First-Time Home Buyers

For many first-time home buyers, GST/HST on newly constructed homes can represent a significant additional cost during the purchase process.

In 2025 and 2026, new federal and proposed provincial rebate programs were introduced to help eligible first-time home buyers reduce the tax burden associated with purchasing newly built homes, substantially renovated homes, and some owner-built properties.

Understanding how these rebates work can help buyers make more informed financial decisions before entering into agreements with builders or beginning construction projects.

This article provides an overview of:

- Federal GST/HST new housing rebates

- First-time home buyer GST/HST rebates

- Ontario rebate considerations

- Eligibility requirements

- Rebate calculations

- Important restrictions

- Assignment sale considerations

- Owner-built home eligibility

- Application timing and documentation

How Much Could You Save?

What Is the First-Time Home Buyer GST/HST Rebate?

The First-Time Home Buyer (FTHB) GST/HST rebate is intended to reduce or eliminate some of the GST or HST payable on qualifying newly constructed homes.

The rebate generally applies to:

- Newly built homes purchased from a builder

- Substantially renovated homes

- Some owner-built homes

- Certain co-operative housing purchases

The rebate applies only to qualifying transactions and strict eligibility requirements must be met.

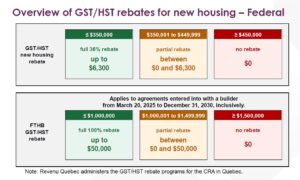

Federal GST/HST Rebate Overview

Existing GST/HST New Housing Rebate

The existing federal GST/HST New Housing Rebate currently provides:

| Purchase Price | Federal Rebate |

|---|---|

| Up to $350,000 | Full rebate up to $6,300 |

| $350,001 – $449,999 | Partial rebate |

| $450,000+ | No rebate |

The rebate gradually phases out between $350,000 and $450,000.

Enhanced First-Time Home Buyer GST/HST Rebate

The enhanced federal first-time home buyer rebate introduced for agreements entered into from March 20, 2025 to December 31, 2030 provides significantly larger potential rebates.

Federal Rebate Thresholds

| Purchase Price | Rebate Availability |

| Up to $1,000,000 | Full rebate up to $50,000 |

| $1,000,001 – $1,499,999 | Partial rebate |

| $1,500,000+ | No rebate |

This expanded rebate structure is particularly important in higher-priced housing markets such as Toronto and the Greater Toronto Area.

Who Qualifies as a First-Time Home Buyer?

To qualify as a first-time home buyer, an individual generally must meet all of the following conditions:

Age Requirement

The buyer must be at least 18 years old.

Citizenship or Residency

The buyer must be:

- A Canadian citizen, or

- A permanent resident of Canada.

Prior Home Ownership Restrictions

The buyer must not have occupied a home they owned, either solely or jointly, as their primary residence during:

- the current calendar year, or

- the previous four calendar years.

Spouse or Common-Law Partner Rules

If the buyer has a spouse or common-law partner, the same ownership and occupancy restrictions may also apply to the spouse or partner.

When Is “First-Time Buyer” Status Determined?

The legislation uses what is called a “particular time” test.

The relevant timing depends on the type of purchase:

| Transaction Type | Relevant Time |

| Purchase from builder (building and land) | When ownership transfers |

| Purchase on leased land | When possession transfers |

| Co-op purchase | When ownership transfers |

| Owner-built home | Earlier of occupancy or substantial completion |

This timing issue can become extremely important where buyers recently sold homes, changed marital status, or are involved in assignment transactions.

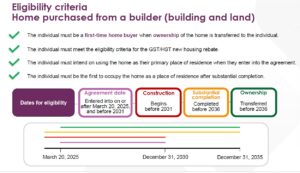

Eligibility Requirements for Builder Purchases

For newly built homes purchased directly from a builder, several additional requirements apply.

The buyer must:

- qualify as a first-time home buyer,

- meet GST/HST new housing rebate eligibility,

- intend to use the property as their primary residence,

- and be the first occupant after substantial completion.

Additional timing requirements include:

| Requirement | Deadline |

| Agreement entered into | March 20, 2025 – Dec 31, 2030 |

| Construction begins | Before 2031 |

| Substantial completion | Before 2036 |

| Ownership transfer | Before 2036 |

Federal Rebate Calculation Examples

Homes Up To $1,000,000

Eligible buyers may receive:

- up to 100% of GST paid,

- to a maximum rebate of $50,000.

Homes Between $1,000,001 and $1,499,999

The rebate phases out proportionally using the CRA formula:

A\times\frac{(1,500,000-B)}{500,000}

Where:

- A = total GST paid (up to $50,000)

- B = total consideration (purchase price)

Homes $1,500,000 and Above

No federal first-time home buyer GST/HST rebate is available.

Example Federal Rebate Calculations

| Purchase Price | GST Paid (5%) | FTHB Rebate |

| $450,000 | $22,500 | $22,500 |

| $1,000,000 | $50,000 | $50,000 |

| $1,250,000 | $62,500 | $25,000 |

| $1,500,000 | $75,000 | $0 |

Ontario New Housing Rebates

Ontario currently provides a separate Ontario New Housing Rebate (ON NHR), which may reimburse:

- 75% of the provincial portion of HST paid,

- up to a maximum rebate of $24,000.

The CRA materials also reference proposed enhanced Ontario rebate programs for first-time home buyers and higher-value housing. These proposed rebates were noted as not yet law and subject to change at the time of publication.

Because provincial rebate programs may change, buyers should verify current eligibility rules before relying on projected rebate amounts.

Owner-Built Homes

The rebate program may also apply to owner-built homes and substantial renovations.

Generally, the buyer must:

- qualify as a first-time home buyer,

- intend to use the property as their primary residence,

- and be the first occupant after substantial completion.

Construction or renovation must generally:

- begin on or after March 20, 2025,

- begin before 2031,

- and be substantially completed before 2036.

Important Restrictions and Risk Considerations

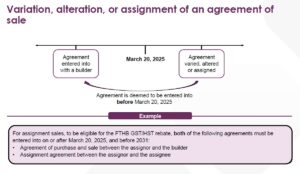

Assignment Sales

Assignment transactions involve additional risk and eligibility concerns.

For an assignment transaction to qualify:

- the original agreement with the builder,

- and the assignment agreement,

must both generally be entered into after March 20, 2025 and before 2031.

Improperly structured assignment transactions may create rebate ineligibility.

Groups of Purchasers

Where multiple individuals purchase together:

- at least one purchaser must qualify as a first-time home buyer,

- and the individual claiming the rebate must qualify personally.

Corporations are not eligible for the rebate.

Spousal Restrictions

An individual generally cannot receive the rebate if:

- they previously received the rebate, or

- their spouse or common-law partner previously received it.

These rules can become complicated in joint purchase structures.

Construction Timing Issues

For owner-built homes, “construction commencement” is important.

The CRA materials indicate that construction generally begins when excavation work begins.

Where construction stops and later resumes, the original excavation date may still control eligibility timing.

Practical Considerations for Buyers

Before relying on projected GST/HST rebates, buyers should carefully review:

- builder agreements,

- assignment provisions,

- occupancy dates,

- intended use requirements,

- closing adjustments,

- and ownership structures.

Many rebate disputes occur because:

- agreements are amended,

- purchasers are added or removed,

- occupancy changes,

- assignments are improperly structured,

- or buyers misunderstand primary residence requirements.

Professional review before signing can help reduce avoidable issues later.

Final Thoughts

The enhanced first-time home buyer GST/HST rebate programs may provide substantial savings for qualifying purchasers of newly built homes.

In higher-priced markets, these rebates can significantly affect:

- affordability,

- down payment planning,

- closing costs,

- and long-term financing considerations.

However, eligibility rules are highly technical and timing-sensitive.

Before entering into agreements with builders or assignment sellers, buyers should carefully review:

- eligibility requirements,

- ownership structures,

- rebate assumptions,

- and assignment implications.

Proper transaction structure and documentation may help avoid unexpected tax exposure or lost rebate opportunities later.

Click here for a copy of Canada Revenue Agency’s (CRA) information on the First Time Home Buyers’ GST/HST Rebates.

Disclaimer

This article is intended for general informational purposes only and should not be considered accounting, legal, or tax advice. Buyers should consult qualified accounting, legal, and tax professionals regarding their specific circumstances before relying on rebate eligibility or projected rebate amounts.

Written by Rodney Harvey, Broker of Record at Konfidis, Brokerage providing advisory-focused commercial, industrial, investment, and real estate brokerage services across Oshawa, Durham Region, and Ontario.

Related Articles & Resources

What Sophisticated Investors Look for Before Buying Property in Durham Region

What Sophisticated Investors Look for Before Buying Property in Durham Region

Understanding Cap Rates in Durham Region

7 Mistakes Buyers Make When Purchasing Investment Property in Oshawa

Assignment Sales and GST/HST Implications in Ontario

What Investors Should Know Before Creating a Second Suite in Ontario

Calculating Rental Property Profit in Ontario

What Do You Need to Know Before Buying Multi-Family Real Estate?

Put my expertise to work for you!

“If you require professional guidance regarding representation structure, transaction strategy, commercial leasing, investment property, due diligence, or real estate advisory services, consultation and representation options may be available depending on your objectives and circumstances.”